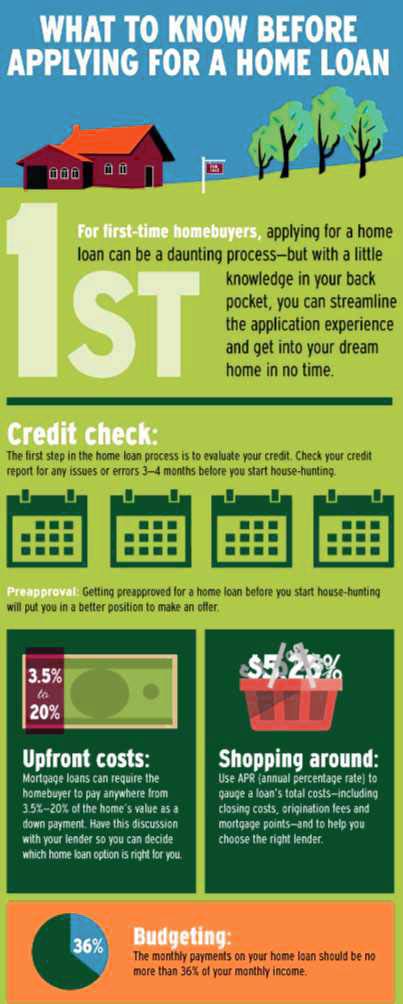

Tip: Check your credit score early.

Your credit score has a major impact on mortgage rates. Review it months before applying so you have time to improve it.

Tip: Shop multiple lenders. Comparing offers from at least three lenders can save you thousands over the life of your mortgage.

Understand fixed vs. adjustable-rate mortgages. Fixed-rate mortgages offer stability, while adjustable-rate mortgages may start lower but carry future rate risk.

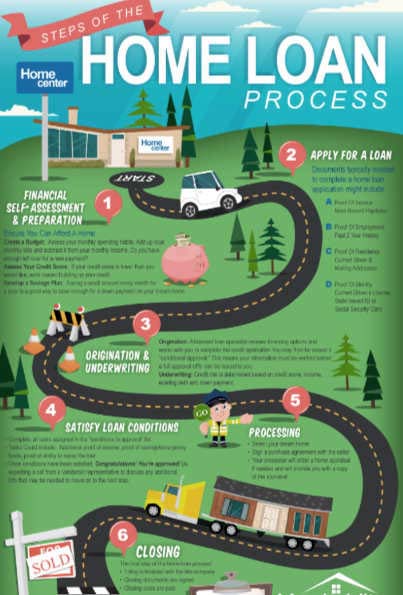

Get pre-approved, not just pre-qualified.

A mortgage pre-approval strengthens your offer and gives you a realistic budget.

Watch the annual percentage rate (APR).

The APR reflects the true cost of a mortgage, including fees—not just the interest rate.

Know your loan options.

FHA, VA, USDA, and conventional loans each have different requirements and benefits.

Factor in total homeownership costs.

Include property taxes, insurance, HOA fees, and maintenance—not just the monthly payment.

Consider points carefully.

Buying discount points can lower your interest rate, but only makes sense if you plan to stay long enough.

Refinance strategically.

Refinancing can lower your rate or payment, but closing costs must justify the savings.

Tip: Check your credit score early.

Your credit score has a major impact on mortgage rates. Review it months before applying so you have time to improve it.

Increase your savings rate with raises.

Treat pay increases as an opportunity to save more, not spend more.

Understand how interest compounds.

Compounding works for you with savings and against you with debt—time matters.

Diversify your investments.

Avoid putting all your money into one asset or market sector.

Finanicial Tip: Build an emergency fund first.

Aim for 3–6 months of expenses to avoid relying on high-interest debt.

Automate your savings.

Automatic transfers make consistent saving easier and more effective.

Pay down high-interest debt aggressively.

Credit card interest often outweighs most investment returns.

Stick to a realistic budget.

A sustainable budget is one you can follow consistently—not one that’s overly restrictive.

Review your finances annually.

Revisit goals, interest rates, insurance, and subscriptions at least once a year.

Avoid lifestyle inflation.

Keeping expenses stable as income grows accelerates wealth building.

Focus on long-term financial decisions.

Sustainable wealth is built through consistent habits, not short-term wins.